The next financial crisis is now waiting in the wings as the Obama administration refuses to push real controls on the financial giants

Susan Ohanian's Comment: I'm posting the article below because Matt Taibbi is so on-target with this comment about the poseurs in Congress. Their lack of knowledge about education is just as stunning and, in the long run, probably even more devastating. Warning: There is "language" here. The article in question is "Wall Street's Big Win," Publication Date: 2010-08-06, By Matt Taibbi, from Rolling Stone, Aug. 6, 2010.

Taibbi: "During an other-wise deathly boring year spent covering this debate, I learned to derive some entertainment from watching politicians scramble to give floor speeches about financial reform without disclosing the fact that they didn't have the first fucking clue what a credit-default swap is, or how a derivative works. This was certainly true of Democrats, but the Republicans were way, way better at it. Their strategy was brilliant in its simplicity: Don't even bother trying to figure out the math-y stuff, and instead just blame the entire crisis on government efforts to make homeowners of lazy black people. "Private enterprise mixed with social engineering" was how Sen. Richard Shelby of Alabama put it, with a straight face, not long before the bill passed..."

And this: ". . . the basic con of congressional politics. Throughout the debate over finance reform, Democrats had sold the public on the idea that it was the Republicans who were killing progressive initiatives. In reality, Republican and Democratic leaders were working together with industry insiders and deep-pocketed lobbyists to prevent rogue members like Merkley and Levin from effecting real change. In public, the parties stage a show of bitter bipartisan stalemate. But when the cameras are off, they fuck like crazed weasels in heat..."

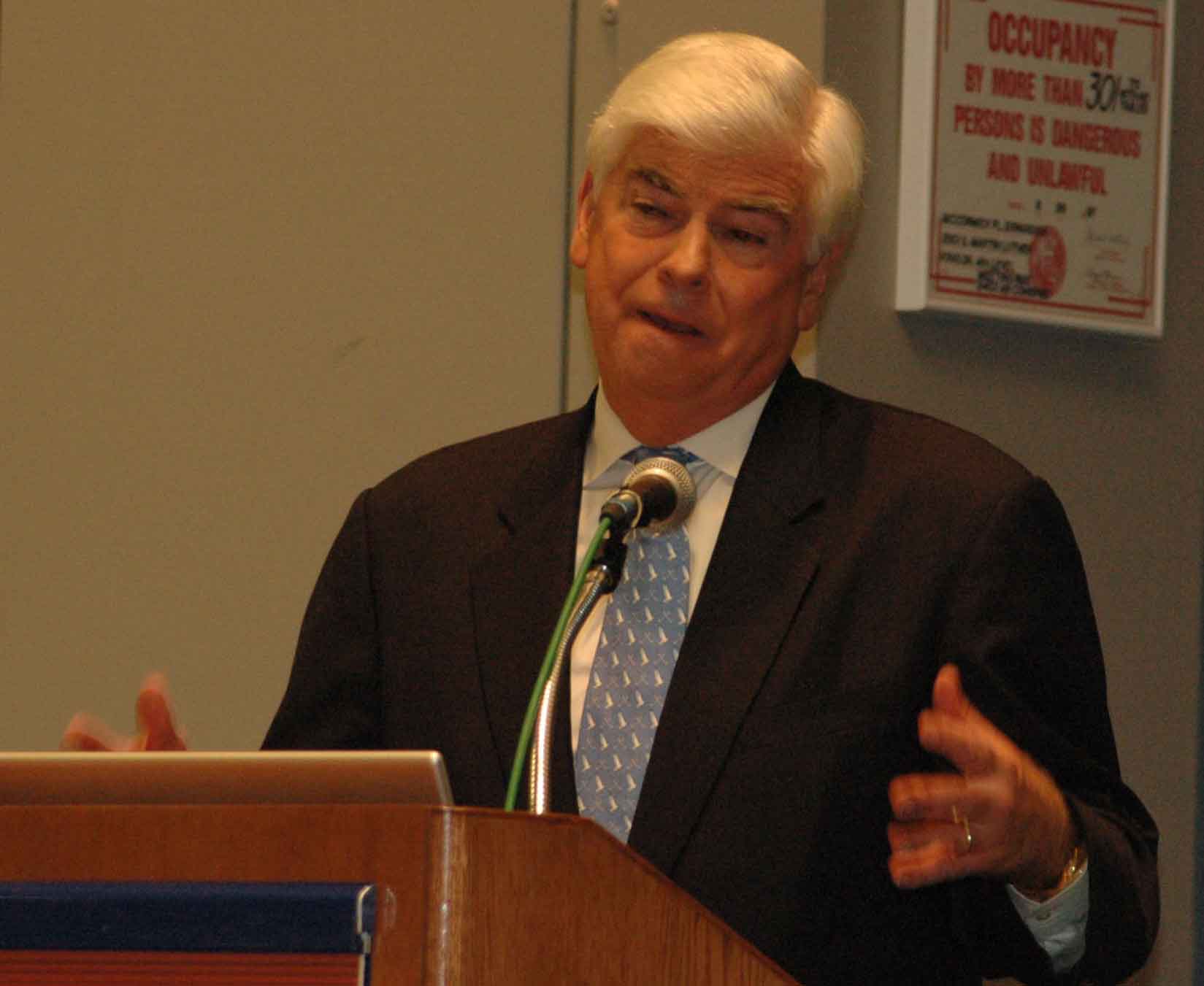

Senator Christopher Dodd speaking in Chicago on August 4, 2007 at the Yearly Kos convention was behind the efforts by Democratic Party leaders to gut any serious reform of the big banks during the past few months. Substance photo by George N. Schmidt.It's also interesting that two laws transforming Wall Street into a giant casino were passed during Bill Clinton's presidency. Public schools now operate under the weight of Clinton's legacy. As Arkansas governor he partnered with Lou Gerstner to bring in America 2000 for Pres. Bush the elder, and then as President his Goals 2000 became a strong precursor to NCLB. Clinton didn't win his fight for national standards and a national test, but we can thank Republican opposition for this delay, which Obama/Duncan are now bringing to fruition.

Senator Christopher Dodd speaking in Chicago on August 4, 2007 at the Yearly Kos convention was behind the efforts by Democratic Party leaders to gut any serious reform of the big banks during the past few months. Substance photo by George N. Schmidt.It's also interesting that two laws transforming Wall Street into a giant casino were passed during Bill Clinton's presidency. Public schools now operate under the weight of Clinton's legacy. As Arkansas governor he partnered with Lou Gerstner to bring in America 2000 for Pres. Bush the elder, and then as President his Goals 2000 became a strong precursor to NCLB. Clinton didn't win his fight for national standards and a national test, but we can thank Republican opposition for this delay, which Obama/Duncan are now bringing to fruition.

Finance reform won't stop the high-risk gambling that wrecked the economy — and Republicans aren't the only ones to blame.

By Matt Taibbi

Cue the credits: the era of financial thuggery is officially over. Three hellish years of panic, all done and gone — the mass bankruptcies, midnight bailouts, shotgun mergers of dying megabanks, high-stakes SEC investigations, all capped by a legislative orgy in which industry lobbyists hurled more than $600 million at Congress. It all supposedly came to an end one Wednesday morning a few weeks back, when President Obama, flanked by hundreds of party flacks and congressional bigwigs, stepped up to the lectern at an extravagant ceremony to sign into law his sweeping new bill to clean up Wall Street.

Obama's speech introducing the massive law brimmed with celebratory finality. He threw around lofty phrases like "never again" and "no more." He proclaimed the end of unfair credit-card-rate hikes and issued a fatwa on abusive mortgage practices and the shady loans that helped fuel the debt bubble. The message was clear: The sheriff was padlocking the Wall Street casino, and the government was taking decisive steps to unfuck our hopelessly broken economy.

But is the nightmare really over, or is this just another Inception-style trick ending? It's hard to figure, given all the absurd rhetoric emanating from the leadership of both parties. Obama and the Democrats boasted that the bill is the "toughest financial reform since the ones we created in the aftermath of the Great Depression" -- a claim that would maybe be more impressive if Congress had passed any financial reforms since the Great Depression, or at least any that didn't specifically involve radically undoing the Depression-era laws.

The Republicans, meanwhile, were predictably hysterical. They described the new law — officially known as the Dodd-Frank Wall Street Reform and Consumer Protection Act — as something not far from a full-blown Marxist seizure of the means of production. House Minority Leader John Boehner shrieked that it was like "killing an ant with a nuclear weapon," apparently forgetting that the ant crisis in question wiped out about 40 percent of the world's wealth in a little over a year, making its smallness highly debatable.

But Dodd-Frank was neither an FDR-style, paradigm-shifting reform, nor a historic assault on free enterprise. What it was, ultimately, was a cop-out, a Band-Aid on a severed artery. If it marks the end of anything at all, it represents the end of the best opportunity we had to do something real about the criminal hijacking of America's financial-services industry. During the yearlong legislative battle that forged this bill, Congress took a long, hard look at the shape of the modern American economy — and then decided that it didn't have the stones to wipe out our country's one dependably thriving profit center: theft.

Tim Dickinson blogs about all the news that fits from the Beltway and beyond on the National Affairs blog.

It's not that there's nothing good in the bill. In fact, there are many good things in it, even some historic things. Sen. Bernie Sanders and others won a fight to allow Congress to audit the Fed's books for the first time ever. A new Consumer Financial Protection Bureau was created to protect against predatory lending and other abuses. New lending standards will be employed in the mortgage industry; no more meth addicts buying mansions with credit cards. And in perhaps the biggest win of all, there will be new rules forcing some varieties of derivatives — the arcane instruments that Warren Buffett called "financial weapons of mass destruction" — to be traded and cleared on open exchanges, pushing what had been a completely opaque market into the light of day for the first time.

All of this is great, but taken together, these reforms fail to address even a tenth of the real problem. Worse: They fail to even define what the real problem is. Over a long year of feverish lobbying and brutally intense backroom negotiations, a group of D.C. insiders fought over a single question: Just how much of the truth about the financial crisis should we share with the public? Do we admit that control over the economy in the past dec ade was ceded to a small group of rapacious criminals who to this day are engaged in a mind- numbing campaign of theft on a global scale? Or do we pretend that, minus a few bumps in the road that have mostly been smoothed out, the clean-hands capitalism of Adam Smith still rules the day in America? In other words, do people need to know the real version, in all its majestic whorebotchery, or can we get away with some bullshit cover story?

Above, Senator Christopher Dodd is one of the main Democratic Party leaders who do the bidding of the nation's largest and most crooked financial institutions. Substance photo by George N. Schmidt.In passing Dodd-Frank, they went with the cover story.

Above, Senator Christopher Dodd is one of the main Democratic Party leaders who do the bidding of the nation's largest and most crooked financial institutions. Substance photo by George N. Schmidt.In passing Dodd-Frank, they went with the cover story.

During an other-wise deathly boring year spent covering this debate, I learned to derive some entertainment from watching politicians scramble to give floor speeches about financial reform without disclosing the fact that they didn't have the first fucking clue what a credit-default swap is, or how a derivative works. This was certainly true of Democrats, but the Republicans were way, way better at it. Their strategy was brilliant in its simplicity: Don't even bother trying to figure out the math-y stuff, and instead just blame the entire crisis on government efforts to make homeowners of lazy black people.

"Private enterprise mixed with social engineering" was how Sen. Richard Shelby of Alabama put it, with a straight face, not long before the bill passed.

The argument favored by Wall Street lobbyists and Obama's team of triangulating pro-business Democrats was more subtle. In this strangely metaphysical version of recent history, the economy was ruined by bad luck and a few bad actors, not by any particular law or policy. It was the "guns don't kill people, people kill people" argument expanded to cover global financial fraud. "There is an assumption that math is evil," insisted Keith Hennessey, a member of the Financial Crisis Inquiry Commission, at a hearing in June. "Credit-default swaps are things, and things can't be culprits."

Both of these takes were engineered to avoid an uncomfortable political truth: The huge profits that Wall Street earned in the past decade were driven in large part by a single, far-reaching scheme, one in which bankers, home lenders and other players exploited loopholes in the system to magically transform subprime home borrowers into AAA investments, sell them off to unsuspecting pension funds and foreign trade unions and other suckers, then multiply their score by leveraging their phony-baloney deals over and over. It was pure financial alchemy — turning manure into gold, then spinning it Rumpelstiltskin-style into vast profits using complex, mostly unregulated new instruments that almost no one outside of a few experts in the field really understood. With the government borrowing mountains of Chinese and Saudi cash to fight two crazy wars, and the domestic manufacturing base mostly vanished overseas, this massive fraud for all intents and purposes was the American economy in the 2000s; we were a nation subsisting on an elaborate check- bouncing scheme.

And it was all made possible by two major deregulatory moves from the Clinton era: the Gramm-Leach-Bliley Act of 1999, which allowed investment banks, insurance companies and commercial banks to merge, and the Commodity Futures Modernization Act of 2000, which exempted the entire derivatives market from federal regulation.

Together, these two laws transformed Wall Street into a giant casino, allowing commercial banks to act like high-risk hedge funds, with a whole new galaxy of derivative bets to lay action on. In fact, the laws made Wall Street even crazier than a casino, because in a casino you have to put up actual money to make bets. But thanks to deregulation, financial companies like AIG could bet billions, if not trillions, without having any money at all to back up their gambles.

Dodd-Frank was never going to be a meaningful reform unless these two fateful Clinton-era laws commercial banks gambling with taxpayer money, and unregulated derivatives being traded in the dark were reversed. The story of how the last real shot at reining in Wall Street got routed tells you everything you need to know about how, and on whose behalf, our government works. It was Congress at its most cowardly, deceptive best, with both parties teaming up to subject reform to death by a thousand paper cuts — with the worst cuts coming, literally, in the final moments before the bill's passage.

The first of the two final battles coalesced around an effort by Sens. Carl Levin of Michigan and Jeff Merkley of Oregon to implement the so-called "Volcker rule," a proposal designed to restore the firewall between investment houses and commercial banks. At the heart of Merkley-Levin was one key section: a ban on proprietary trading.

"Prop trading" is just a fancy term for banks gambling in the market for their own profit. Thanks to the Clinton-era deregulation, giant commercial banks like JP Morgan Chase were not only allowed to serve as investment banks, accumulating mountains of privileged insider information, they were allowed to play the markets themselves. That meant that the prop-trading desk at Goldman Sachs could bet heavily against Greek debt not long after the bank had saddled Greece with toxic interest-rate swaps. It also meant that if any of these "too big to fail" banks went bust, American taxpayers would be expected to bail them out. The Volcker rule — pushed by Paul Volcker, the former Fed chief and current Obama adviser — aimed to lay down a simple law for big banks: If you want to gamble like a drunken sailor, fine. Just don't expect us to mop up the mess after you puke your guts out.

If Obama's team had had their way, last month's debate over the Volcker rule would never have happened. When the original version of the finance- reform bill passed the House last fall — heavily influenced by treasury secretary and noted pencil-necked Wall Street stooge Timothy Geithner — it contained no attempt to ban banks with federally insured deposits from engaging in prop trading. But that changed when Scott Brown, the Tea Party darling from Massachusetts, blindsided the Democrats by wresting away the seat of deceased liberal icon Ted Kennedy. With voters seething over Wall Street's rampant thievery and fraud, the Democrats suddenly got religion about reckless gambling by the financial industry.

Brown won his election on January 19th; just two days later, on January 21st, President Obama pulled a 180 and announced his support for the Volcker rule. Throughout the reform process, Volcker — a legendary figure whose demands for greater responsibility and transparency have alarmed Wall Street — had been forced to take a back seat to Geithner, at one point even sharply criticizing the House bill in open testimony. For the White House to suddenly throw its weight behind Volcker took the Hill by surprise. It was a "complete change of policy — a fundamental shift," observed Simon Johnson, an MIT economist and noted financial analyst.

This was clearly the administration's attempt to get back on the right side of populist anger at Wall Street. So when Merkley and Levin took up the job of transforming Volcker's proposal into legislative reality, they assumed the Democratic leadership would be on their side.

It didn't work out that way. The counter attack began in May, when the Republicans objected to Merkley-Levin and invoked the Senate's unanimous-consent rule, by which no amendment comes to the floor unless all 100 members agree to let it be voted on. That left the Volcker rule in legislative purgatory right up to the initial Senate vote on the bill. In interviews, the soft-spoken, gregarious Merkley steadfastly refuses to point the finger at the Democratic leadership for failing to break the legislative logjam. But reading between the lines, it's obvious that he and Levin were on their own — no one with any juice in the key committees lifted a finger to help them. The two senators were like underage geeks who'd been told by Majority Leader Harry Reid that they had to come up with their own keg if they wanted to come to the party.

But come up with a keg they did. On the week of the first Senate vote, Merkley's staffers pored over Senate procedural rules and discovered an arcane clause that allowed them to attach their proposal to an amendment by Republican Sam Brownback of Kansas designed to exempt auto dealers from regulation by the new Consumer Financial Protection Bureau. The Brownback amendment had already been approved for a vote, so once Merkley's people used the remora-fish tactic of sticking to Brownback, there was seemingly no way to prevent Merkley-Levin from going to a vote. Or so they thought.

"We were plumbing the inner rules of the Senate," Merkley says. One of those rules is that when you attach your amendment to another, your measure has to be "germane" to the amendment you're attaching it to. Since Merkley-Levin's ban on prop trading and Brownback's auto-dealer exemption were completely different, this was not a simple thing to accomplish. So Merkley and Levin personally trekked down to one of the more obscure offices in the congressional complex. "Carl Levin and I went on a trip down to the parliamentarian's office, where I'd never been," Merkley says. "They briefed us on what it took, and the team set about to make it work."

From there, Merkley and Levin hit the phones to lobby other members, including Republicans. Right up to the final vote on May 20th, they thought they had a real shot. "I got the sense that we might pick up quite a few Republican votes," says Merkley. "It was starting to look pretty good."

But that very fact that the Merkley-Levin amendment had such momentum is ultimately what did it in. "What killed us," says Merkley, "was that it was looking pretty good." What happened next was a prime example of the basic con of congressional politics. Throughout the debate over finance reform, Democrats had sold the public on the idea that it was the Republicans who were killing progressive initiatives. In reality, Republican and Democratic leaders were working together with industry insiders and deep-pocketed lobbyists to prevent rogue members like Merkley and Levin from effecting real change.

In public, the parties stage a show of bitter bipartisan stalemate. But when the cameras are off, they fuck like crazed weasels in heat. With Merkley-Levin looking like a good bet to pass, the Republicans pulled a dual-suicide maneuver. Brownback withdrew his auto-dealer exemption, which instantly killed the ban on prop trading. What Merkley and Levin didn't know was that Brownback had worked out an agreement with the Democratic leadership to surreptitiously restore his auto-dealer exemption later on, when the final bill was reconciled with the House version. In other words, Democratic leaders had teamed up with Republicans behind closed doors to double- cross Merkley and Levin.

When the agreement was announced one day before the Senate vote, Merkley couldn't even make sense of what he was hearing. "You're sitting there trying to understand what kind of deal has been struck," he says. "You know there's something there, but you're not really sure."

Merkley almost objected to the deal, but unable to grasp that he had been sold out by his own party's leadership, he hesitated — a fatal mistake. The deal to reinstate Brownback went through, and Merkley's amendment to rein in Wall Street died. That might have been the end of the Volcker rule — but soon after, Merkley and Levin made the most of their one last chance. According to Merkley, he and Levin convinced Rep. Barney Frank, who was overseeing the House bill, to reintroduce the amendment in conference talks. The Volcker rule was alive again but it now began a journey into a new sort of hell, in which insiders from both parties chipped away at it until there was almost nothing left.

It started with Senate rookie Scott Brown, who demanded major changes to Merkley-Levin on behalf of big Massachusetts banks in exchange for his vote. But Senate sources I talked to insist that Chris Dodd, the powerful chair of the Senate Banking Committee, was just using Brown as a cover to gut the Volcker rule.

"It became far more than accommodating the Massachusetts banks," says one high- ranking Senate aide. "It became a ruse for Treasury trying to get as far as they could, with Dodd's help." From the start, Dodd had been opposed to the ban on proprietary trading. "Hey, I would gladly dump the Volcker rule," he told industry lobbyists. "But I can't, because of the pressure I'm getting from the left."

Now, with Brown pressing for concessions, Dodd agreed to let Merkley-Levin be spattered with a wave of loopholes. If you can imagine a 4,000-pound lizard pretending to cower before a Cub Scout clutching a lollipop, then you've grasped the basic dynamic of a grizzled legislative titan like Dodd caving into Brown, the cheery GOP newbie with the Pez- dispenser face.

First, in what amounted to an open handout to the financial interests represented by Brown, insurers, mutual funds and trusts were exempted from the Merkley-Levin ban. Then, with the floodgates officially open, every financial company in America was granted a massive loophole — one that allowed them to skirt the ban on risky gambling by investing a designated percentage of their holdings in hedge funds and private-equity companies.

The common justification for this loophole, known as the de minimis exemption, was that banks need it to retain their "traditional businesses" and remain competitive against hedge funds. In other words, Congress must allow banks to act like hedge funds because otherwise they'd be unable to compete with hedge funds in the hedge-fund business. With the introduction of the de minimis exemption, Merkley-Levin went from being an absolute ban on federally insured banks engaging in high-risk speculation to a feeble, half-assed restriction that will be difficult, if not impossible, to enforce.

The driving force behind the exemption was not Scott Brown, but the Obama administration itself. By all accounts, Geithner lobbied hard on the issue. "Treasury's official position went from opposed to supportive," one aide told reporters. "They may have even overshot Brown's desires by a bit."

Throughout the negotiations over the bill, in fact, Geithner acted almost like a liaison to the financial industry, pushing for Wall Street-friendly changes on everything from bailouts (his initial proposal allowed the White House to unilaterally fork over taxpayer money to banks in unlimited amounts) to high-risk investments (he fought to let megabanks hold on to their derivatives desks). Geithner went all out for the de minimis exemption; one Senate aide was told flatly by "those who are in charge of counting noses" that the proposal was not subject to negotiation.

This was the horse-head-in-the-bed moment of the Dodd-Frank bill the offer that couldn't be refused. "We were told that there needed to be de minimis or there would be no bill," the aide says. When Merkley first got the news about the exemption, he tried to keep it small. "I was hoping to limit it to one percent" of a company's tangible equity, he says. "The night before the conference, Geithner was pushing for two percent. In the end, it got even worse — it was three percent."

When Merkley tried to put a specific dollar limit of $250 million on high-risk gambling, Geithner shot him down. "He didn't want the sub-cap, and we lost," Merkley says. Still, during the last round of negotiations, Merkley and Levin managed to pare back some of the worst of the exemptions. In one victory, they eliminated a proposal by Geithner that would have allowed banks to make unlimited trades "in facilitation of customer relations" — a loophole so laughably broad that it would cover, in the words of one Senate aide, "pretty much everything" that banks wanted to do. By June 25th, when the bill headed to its final meeting of the conference committee, it looked like Merkley and Levin would finally get their vote. But that was before the senator from Wall Street showed up.

In the final hours of negotiations, a congressional delegation from New York, led by Sen. Chuck Schumer, decided to take one last run at gutting the Volcker rule. It was as though someone had sent the scrubs off the court and called in the varsity. Schumer, a platitudinous champion of liberal social issues, moonlights as a pillbox-hat bellhop to Wall Street on economic matters. The self- aggrandizing New Yorker has not only fought to keep taxes low on hedge-fund billionaires, he got up onstage with Goldman Sachs CEO Lloyd Blankfein at a Democratic fundraiser in 2006 and performed "nostalgic furniture-store jingles." This bears repeating: The person in whose hands America had placed its hopes for finance reform was someone who once sang furniture jingles onstage with Lloyd Blankfein.

Now, as the bill headed into final negotiations, the Schumer coalition suddenly decided that the de minimis exemption for banks simply wasn't big enough. In a neat trick, Schumer's crew agreed to keep the exemption at three percent but they raised the limit dramatically by making it three percent of something else. Instead of being pegged to a bank's "tangible equity," the exemption would now be calculated based on a financial firm's "Tier 1" capital a far bigger pool of money that includes a bank's common shares and deferred-tax assets instead of just preferred shares.

In real terms, banks could now put up to 40 percent more into high-risk investments. "It was almost double what Geithner was talking about the night before," says Merkley. "For Bank of America alone, it comes to $6 billion." Schumer himself entered the change in the Senate version of the bill — and then asked the House to sign off on it 15 minutes later. Rep. Paul Kanjorski of Pennsylvania, who had worked hard on the Volcker rule, tried to get a vote to block the change. But Barney Frank laid into him. "You had plenty of time with this," Frank barked. "You knew what was coming — siddown."

Thus the Merkley-Levin across-the-board ban on risky proprietary trading became a partial ban in which insurers, mutual funds and trusts are completely exempt, and banks can still gamble three percent of their holdings. In practice, it will be up to future regulators to define how that limit will be calculated — and one can only imagine how far banks like Goldman Sachs will manage to stretch the loopholes in what's left of the Volcker rule.

"It's not a total nothing burger," sighs one aide. "But, by the end, it didn't change a whole lot." If the Volcker rule was a regulatory Godzilla threatening to stomp out Wall Street's self-serving investments, the proposal to shut down derivatives was nothing short of a planet-smashing asteroid headed straight at the heart of the financial industry's most reckless abuses.

The key battle involved the so-called "Lincoln rule," put forward by Sen. Blanche Lincoln of Arkansas, which would have forced big banks to spin off their derivatives desks in the same way the Volcker rule would have forced them to give up proprietary trading. Banks would have to make a choice: Either forgo access to the cheap cash of the Federal Reserve, or give up gambling with dangerous instruments like credit-default swaps. Banks, in short, would have to go back to making money the old-fashioned way — making smart loans, underwriting new businesses, earning simple fees on customer trades. No more leveraged gambling on whacked-out acid-trip derivatives deals, no more walking around with torches and taking out fire insurance on other people's houses, no more running up huge markers on the taxpayer's dime.

This, obviously, could not be permitted. Thanks to Clinton-era deregulation, the market for derivatives is now 100 times larger than the federal budget, and five of the country's biggest banks control more than 90 percent of the business.

So the leadership of both parties pulled out all the stops to ensure that the Lincoln rule would be Swiss-cheesed to death before it ever saw the light of day. The effort began with an extraordinary scene on the floor of the Senate — one that testifies to the nearly unanimous respect that senators hold for the human loophole machine known as Chris Dodd. In late May, the week the Senate voted on its version of the bill, Dodd came up with a hastily composed, five-page substitute to the Lincoln rule that would create a "financial stability" council with the power to unilaterally kill the rule.

Faced with opposition from members of his own party, Dodd agreed to withdraw his substitute two days before the Senate vote — but given his track record of legislative maneuvering on behalf of big banks, his fellow Democrats weren't about to take him at his word. A group of senators from Dodd's own party — including Maria Cantwell of Washington — arranged to stay on the Senate floor in shifts, ensuring that there would be someone there to object in case Dodd tried to push his substitute through during one of those quiet, empty-hall, C-SPAN moments when no one was looking.

The fact that a group of Democrats had to come up with a scheme to prevent one of their own leaders from dropping a roofie in their legislative drinks pretty much sums up the state of affairs in Congress. "Yeah, that's the way it went down," says a Senate aide familiar with the Dodd Watch maneuver. With Dodd unable to introduce his plan to gut the Lincoln rule, the measure actually passed in the Senate, to the extreme surprise of almost everyone on the Hill. This was a rare example of the Senate leadership not just allowing a vote on a financial reform guaranteed to cost major campaign contributors billions of dollars, but actually passing it.

But the ink was barely dry on the Senate bill before a full-blown mobilization against the Lincoln rule was under way. Just days after the Senate vote, Barney Frank came out and voiced opposition to the rule, saying it "goes too far." He trotted out Wall Street's lame, catchall justification for unfettered speculation: Banks need derivatives to balance their portfolios and "hedge their own risk."

Not long after, a group of 43 conservative House Democrats calling themselves the "New Democrat Coalition" refused to support the reform bill unless the toughest part of the Lincoln rule — section 716 — was gutted. "They were threatening to vote against the legislation unless accommodations were made for the banks, and the biggest accommodation was watering down 716," says Michael Greenberger, a Clinton-era financial regulator involved in the talks. It seemed like every Democrat who mattered was against 716: Dodd, Frank, the New Democrats, the Treasury department, the influential FDIC chief Sheila Bair, even Paul Volcker. Schumer and other New Yorkers lobbied mightily against it, arguing that it would be a drain on the income of Wall Street banks; New York mayor Michael Bloomberg traveled to Washington specifically to lobby against the Lincoln rule.

But the crowd had turned against Wall Street, and the populist scrubs seemed like they were about to win big. But then Blanche Lincoln, the captain of the scrubs, coughed up the ball. Lincoln, who was never considered a particularly strong advocate of finance reform, had originally proposed her ban on derivatives — the most radical reform in the entire bill — during a re-election campaign in which she faced a stiff populist challenge from Bill Halter, the lieutenant governor of Arkansas.

Rumors circulated in Washington that Democratic leaders were cynically holding off on gutting Lincoln's proposal until she got past Halter in the primary. If that was the plan, it worked. In early June, only a week after she defeated Halter in the runoff, Lincoln set about gutting her own rule. First she offered a broad exemption for community banks. Then a group of conservative House Democrats led by Rep. Collin Peterson of Minnesota proposed an even bigger compromise one that would exempt virtually every type of derivative from federal oversight.

"I was told that Peterson offered this compromise and Lincoln quickly accepted it," says Greenberger. That was the beginning of the end. The new deal allowed banks to keep their derivatives desks by moving them into subsidiary units and exempted whole classes of derivatives from regulation: interest-rate swaps (the culprits in disasters like Greece and Orange County), foreign-exchange swaps (which helped trigger a global crash after Long Term Capital Management imploded in 1998), cleared credit-default swaps (a big contributor to the AIG collapse) and currency swaps (also involved in the Greece mess).

"About 90 percent of the derivatives market was exempted," says Greenberger. In the end, this would be the entire list of derivatives that are subject to the new law: credit- default swaps that have not been cleared by regulators and swaps involving commodities other than silver and gold. Hilariously, even the few new regulations on derivatives that remained in the bill don't seem to worry Wall Street. Just a few weeks after Lincoln agreed to gut the measure, famed JP Morgan executive Blythe Masters, often credited as one of the inventors of the credit-default swap — one insider calls her "the Darth Vader of the swaps market" — actually sounded psyched about the bill. The new law, she declared publicly, won't even hurt energy commodities, one of the few classes of derivatives that Lincoln didn't exempt.

"It's not a big change for commodities," Masters said. "It's fine-tuning more than a material impact." The so-called reforms, she concluded, "are actually going to be very beneficial for the industry."

And that, ladies and gentlemen, is what the Obama administration is touting as the toughest financial reform since the Great Depression. The systematic gutting of both the Lincoln rule and the Volcker rule in the final days before the passage of Dodd-Frank was especially painful, in part, because so many other crucial reforms that would have spoken directly to the Big Fraud had already been whitewashed out of the bill. An amendment mandating the breakup of too-big-to-fail companies got walloped back in May, and Congress even rejected a ban on "naked" credit-default swaps — the financial equivalent of selling somebody a car with crappy brakes and then taking out a life-insurance policy on the driver.

The few reforms that Congress didn't reject outright it simply kicked into a series of "study groups" created by the bill. Along with promised studies on no - brainers like executive compensation and credit-rating agencies, the bill even punts on the fundamental question of how much capital banks should be required to keep on hand as a hedge against meltdowns, leaving the question to the Basel banking conferences in Switzerland later this year, where financial interests from all over the world will gather to hammer things out in inscrutable backroom negotiations.

"The next phase of all this — the regulatory phase — is going to be supertechnical and complex," says one Senate aide. "It raises questions about how journalists are going to keep the public the slightest bit interested. You might as well just hit the snooze button." Worst of all, some analysts warn that the failure to rein in Wall Street makes another meltdown a near-certainty. "Oh, sure, within a decade," said Johnson, the MIT economist. "The question: Is it three years or seven years?"

Johnson was part of a panel sponsored by the nonpartisan Roosevelt Institute — including Nobel Prize-winning economist Joseph Stiglitz and bailout watchdog Elizabeth Warren — that concluded back in March that the reform bill wouldn't do anything to stop a "doomsday cycle." Too-big-to-fail banks, they said, would continue to borrow money to take massive risks, pay shareholders and management bonuses with the proceeds, then stick taxpayers with the bill when it all goes wrong.

"Risk-taking at banks will soon be larger than ever," the panel warned. Without the Volcker rule and the Lincoln rule, the final version of finance reform is like treating the opportunistic symptoms of AIDS without taking on the virus itself. In a sense, the failure of Congress to treat the disease is a tacit admission that it has no strategy for our economy going forward that doesn't involve continually inflating and reinflating speculative bubbles. Which sucks, because what happened to our economy over the past three years, and is still happening to it now, was not an accident or an oversight, but a sweeping crime wave unleashed by a financial industry gone completely over to the dark side. The bill Congress just passed doesn't go after the criminals where they live, or even make what they're doing a crime; all it does is put a baseball bat under the bed and add an extra lock or two on the doors. It's a hack job, a C-minus effort. See you at the next financial crisis.